Make your plan

Nobody is born knowing how to manage their money – it has to be learned. Even if it seems like you don’t have any money at all right now, learning to manage what you do have is the first step to building wealth.

This important skill will continue to evolve and grow as you go through life. Become aware of your money and what you’re doing with it by getting hands-on and your head straight. Using cash, shopping around for the best prices and creating (and maintaining) good credit all can help you, but the most important thing you have going for you is that time is on your side when it comes to saving now.

Give, Invest, Save, Spend

When you get paid, automatically divide your money into separate containers for these categories or have four sub-accounts at your bank – whatever works best for you is what will work when building your budget. This framework can help you keep a balanced focus and allow you to easily build your wealth while achieving your short-term needs and wants.

Once you give, you realize that it doesn’t take much to make a positive difference – it just takes getting inspired to do it in the first place. Good things happen from giving, both to those you help and within yourself. And, when you are giving to a cause you believe in, you’re connecting with people who have similar interests and may ultimately help you find a career doing what you love. Are you an animal lover? Do you get passionate when talking about human rights? Is there a specific need in your neighborhood or community? When you’re considering who to give to, think about your interests, do some online research, or talk to your parents, teachers and friends to find the best fit for you.

Investing for your future isn’t just vital, it’s directly related to your quality of life (health, comfort and happiness). It’s key to your financial independence, and is the money you’ll live on when you’re older. Investments can include things like real estate, stocks, bonds and mutual funds. Luckily for you time is on your side, so not only are you building your knowledge and experience now but you’re more likely to become a competent investor as each year goes by. The more you invest, and the more you learn about how to do it well, the sooner you may be able to reach financial freedom. Start early to get ahead and reach your long-term goals.

There is no assurance that any investment strategy will be successful. Investing involves risk including the possible loss of capital.

Whether for a car, college tuition or a trip, saving gives you the chance to set and achieve your short-term goals. Like with investing, the sooner you start, the better. Here’s where self-control comes in to avoid spending money you don’t have to impress people. Make sure you are the one who really wants what it is you’re looking to buy. Researchers have shown one of the best ways to develop self-control is by saving – and doing so while you’re young is one important indicator of your future financial success. Saving is also related to lower stress levels and can give you greater optimism about all your future holds.

Consider this your checking account that pays for your expenses such as rent, food, transportation, clothes and your cellphone bill. You’ll also want to make sure you set aside some of this money for fun, which is one reason you want to manage this category well. We make so many small decisions each day that relate to everyday spending, so develop good habits now that will help keep you from overspending – which can keep you locked in a vicious cycle of bad debt.

*These are recommended guidelines to follow. Please make sure that you are budgeting for your fixed and variable expenses first.

*The GISS model is a part of the Zela Wela Way.

What are you working with?

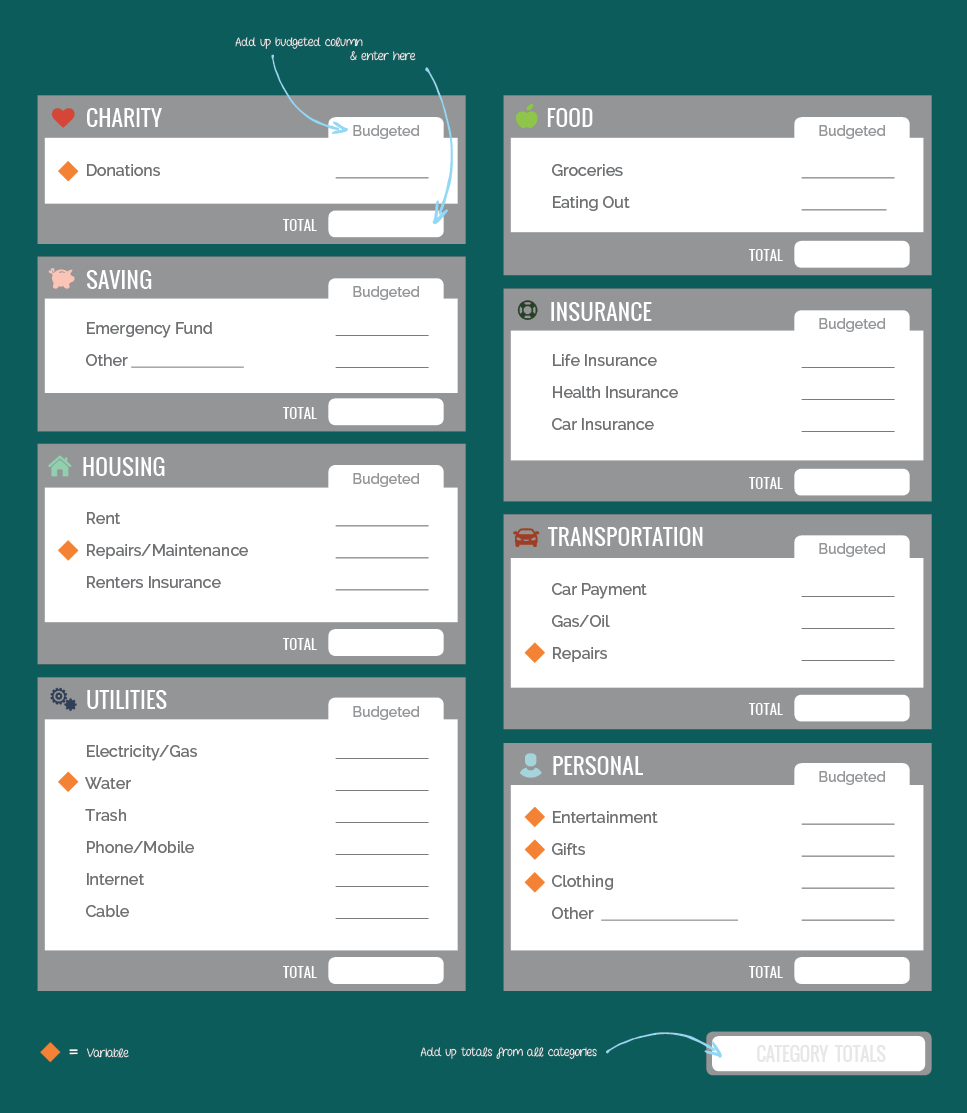

Understanding your spending and where your money is going can help you work toward your short and long-term goals. Download the worksheet below to fill out and plan your monthly budget.

Check out how waiting to save keeps you behind.

Waiting to begin your savings plan can have a huge impact on your results. A delay of even a few years could cost you thousands of dollars. This calculator helps show you how much postponing your savings plan can really cost.

- Starting amount

- The starting balance or current amount you have invested or saved. For this calculator, we assume your current savings is earning your annual rate of return whether you decide to delay your new contributions or not. For example, if you have a current balance of $1000 and never make any new contributions, your delayed and non-delayed results will be the same.

- Additional contributions

- The amount that you plan on adding to your savings or investment each period. The options include monthly, quarterly and annually. This calculator assumes that you make your contributions at the beginning of each period.

- Years

- The total number of years you are planning to save or invest.

- Rate of return

- The annual rate of return for this investment or savings account. The actual rate of return is largely dependent on the types of investments you select. The Standard & Poor's 500® (S&P 500®) for the 10 years ending Dec. 1, 2014, had an annual compounded rate of return of 8.06%, including reinvestment of dividends. From Jan. 1970 through to Dec. 2014, the average annual compounded rate of return for the S&P 500®, including reinvestment of dividends, was approximately 10.7% (source: standardandpoors.com). Since 1970, the highest 12-month return was 61% (June 1982 through June 1983). The lowest 12-month return was -43% (March 2008 to March 2009). Savings accounts at a financial institution may pay as little as 0.25% or less but carry significantly lower risk of loss of principal balances.

It is important to remember that these scenarios are hypothetical and that future rates of return can't be predicted with certainty and that investments that pay higher rates of return are generally subject to higher risk and volatility. The actual rate of return on investments can vary widely over time, especially for long-term investments. This includes the potential loss of principal on your investment. It is not possible to invest directly in an index and the compounded rate of return noted above does not reflect sales charges and other fees that Separate Account investment funds and/or investment companies may charge.

- Years to postpone saving

- The number of years you might wait before you begin saving. We will then delay your new contributions for that number of years.

- Frequency of contributions

- How often you make contributions to your account. The options include monthly, quarterly and annually. This calculator assumes that you make your contributions at the beginning of each period.

- Cost of waiting

- The difference in your savings or investment balance between your delayed and non-delayed plans.

- Required contribution

- If you wait to start saving, this is the amount you would need to contribute each period to achieve the same result as starting your savings plan immediately.

WHATS YOUR PASSION / SET YOUR GOALS / MAKE YOUR PLAN / CRUSH THE MYTHS / Q&A / SHINING ON

© Raymond James & Associates, Inc., member New York Stock Exchange / SIPC|Legal Disclosures|Privacy Policy

Raymond James financial advisors may only conduct business with residents of the states and/or jurisdictions for which they are properly registered. Therefore, a response to a request for information may be delayed. Please note that not all of the investments and services mentioned are available in every state. Investors outside of the United States are subject to securities and tax regulations within their applicable jurisdictions that are not addressed on this site. Contact your local Raymond James office for information and availability.

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website's users and/or members.