The Week in Review: 8/19/24

Don’t think about the start of the race, think about the ending.” – Usain Bolt

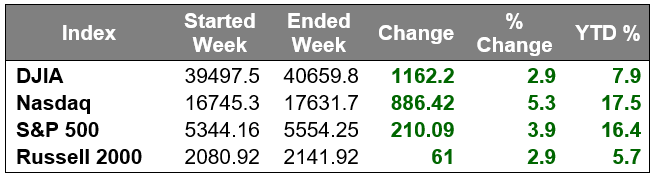

Our stock markets logged solid gains again last week…

The Dow Jones Industrial Average and Russell 2000 each closed 2.9% higher, the S&P 500 jumped 3.9%, and the Nasdaq Composite climbed 5.3%.

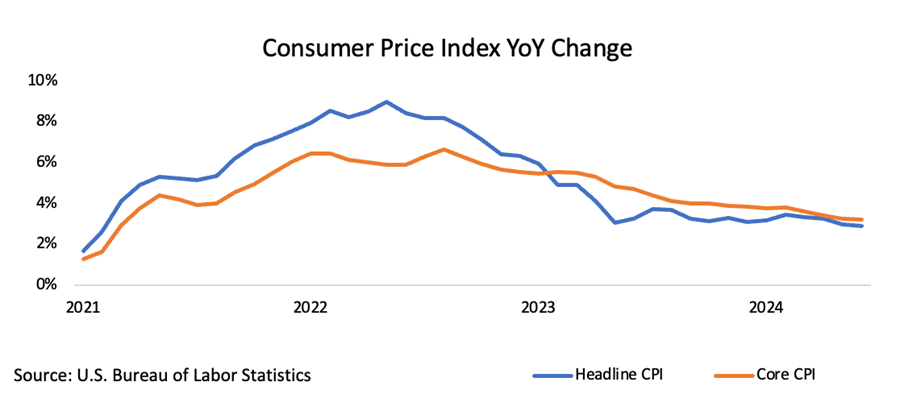

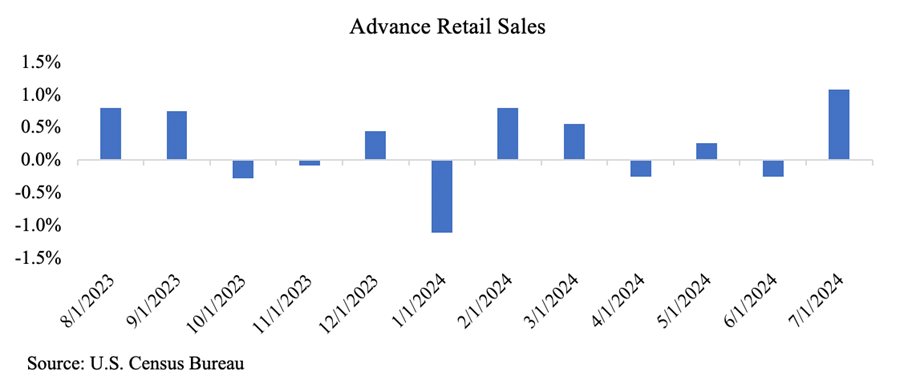

The volatile action we have seen thus far in August was caused by a July jobs report that stirred concerns about a weakening economic environment and labor market. So, last week's release of economic data that had the market feeling good about the economic environment and labor market invited strong buying activity.

The pleasing economic releases included the Producer Price Index for July, which showed disinflation in total and core PPI, the Consumer Price Index for July, which was in-line with expectations, the Retail Sales report for July, which was much better than expected, and the weekly jobless claim report, which reflected ongoing strength in the labor market.

A disappointing housing starts and building permits report for July on Friday didn't deter the strong rally last week.

Solid earnings results and commentary about the consumer from Walmart, along with Cisco's solid fiscal Q4 operating performance, contributed to the upside bias last week.

In other corporate news, Dow component Home Depot closed 3.9% higher last week despite reporting below-consensus guidance.

Starbucks was in the headlines after news that CEO Laxman Narasimhan has stepped down and will be replaced by Chipotle CEO Brian Niccol.

Kellanova also made news after Mars confirmed it will acquire Kellanova for $83.50/share in cash, or total consideration of $35.9 billion, including debt.

Alphabet settled slightly lower in the week despite other mega caps outperforming after a Bloomberg report that the Department of Justice may be looking at breaking up the company following last week's court ruling that Alphabet violated search-related antitrust laws.

All 11 S&P 500 sectors closed higher led by consumer discretionary (+5.2%), information technology (+7.5%), and financials (+3.2%).

Market Snapshot…

- Oil Prices – Oil prices fell last week amid reports Mideast cease fire talks are ongoing. West Texas Intermediate crude was down $1.51 or 1.93% to $76.65 a barrel, while Brent crude futures edged down $1.36, or 1.68% to $79.68 a barrel.

- Gold– Gold prices climbed to an all-time high as the dollar weakened and amid rate cut expectations. Spot gold was up 1.5% to $2,493.66 per ounce. U.S. gold futures rose 1.6% to $2,532.10. Silver finished the week at $29.26.

- U.S. Dollar– As the dollar dropped, investors tried to gauge the Fed’s appetite for interest rate cuts. The dollar was down 0.96% to 147.87. The dollar index slipped 0.35% at 102.67. Euro/US$ exchange rate is now 1.107.

- U.S. Treasury Rates– The U.S. 10-year Treasury yield ticked down 4.3 basis points to 3.883%.

- Asian shares were mixed in overnight trading.

- European markets are trading up.

- Domestic markets are trading higher again this morning.

This week’s feature event will be the Jackson Hole Symposium, hosted by the Kansas City Fed.

The annual event brings together central bankers, economists, academics, government officials, and financial market participants to discuss long-term policy effects and concerns affecting the global marketplace. This year’s theme is “Reassessing the Effectiveness and Transmission of Monetary Policy.”

Based on comments and speeches made during this event, especially Chairman Powell’s, we could get a clearer picture on the Fed’s outlook and anticipated rate cuts. Dovish rhetoric could push markets higher, while hawkish rhetoric could send markets lower.

Have a wonderful week!

The opinions expressed herein are those of Michael Hilger and not necessarily those of Raymond James & Associates, Inc., and are subject to change without notice. The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. There is no assurance any of the trends mentioned will continue or forecasts will occur. The information has been obtained from sources considered to be reliable, but Raymond James does not guarantee that the foregoing material is accurate or complete. Investing involves risk and you may incur a profit or loss regardless of strategy selected.The information contained herein is general in nature and does not constitute legal or tax advice. Inclusion of these indexes is for illustrative purposes only. Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs or other fees, which will affect actual investment performance. Individual investor's results will vary. Past performance does not guarantee future results. The Dow Jones Industrial Average (INDU) is the most widely used indicator of the overall condition of the stock market, a price-weighted average of 30 actively traded blue chip stocks, primarily industrials. The Dow Jones Transportation Average (DJTA, also called the "Dow Jones Transports") is a U.S. stock market index from the Dow Jones Indices of the transportation sector, and is the most widely recognized gauge of the American transportation sector. Standard & Poor's 500 (SPX) is a basket of 500 stocks that are considered to be widely held. The S&P 500 index is weighted by market value, and its performance is thought to be representative of the stock market as a whole. The S&P 500 is an unmanaged index of widely held stocks that is generally representative of the U.S. stock market. Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs and other fees, which will affect investment performance. Individual investor’s results will vary. The NASDAQ Composite Index (COMP.Q) is an index that indicates price movements of securities in the over-the-counter market. It includes all domestic common stocks in the NASDAQ System (approximately 5,000 stocks) and is weighted according to the market value of each listed issue. The NASDAQ-100 (^NDX) is a modified capitalization-weighted index. It is based on exchange, and it is not an index of U.S.-based companies. The Russell 2000 index is an unmanaged index of small cap securities which generally involve greater risks.

U.S. government bonds and Treasury notes are guaranteed by the U.S. government and, if held to maturity, offer a fixed rate of return, and guaranteed principal value. U.S. government bonds are issued and guaranteed as to the timely payment of principal and interest by the federal government. Treasury notes are certificates reflecting intermediate-term (2 - 10 years) obligations of the U.S. government.

The companies engaged in business related to a specific sector are subject to fierce competition and their products and services may be subject to rapit obsolescence. There are additional risks associated with investing in an individual sector, including limited diversification.

Dividends are not guaranteed and must be authorized by the company's board of directors.

Diversification does not ensure a profit or guarantee against a loss.

Investing in oil involves special risks, including the potential adverse effects of state and federal regulation and may not be suitable for all investors.

International investing involves special risks, including currency fluctuations, differing financial accounting standards, and possible political and economic volatility.

The companies engaged in the communications and technology industries are subject to fierce competition and their products and services may be subject to rapid obsolescence.

Gold is subject to the special risks associated with investing in precious metals, including but not limited to: price may be subject to wide fluctuation; the market is relatively limited; the sources are concentrated in countries that have the potential for instability; and the market is unregulated.

The information contained within this commercial email has been obtained from sources considered reliable, but we do not guarantee the foregoing material is accurate or complete.

Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Prior to making an investment decision, please consult with your financial advisor about your individual situation.

Charts are reprinted with permission, further reproduction is strictly prohibited.

If you would like to be removed from this e-Mail Alert Notification, PLEASE click the Reply button, type "remove" or "unsubscribe" in the subject line and include your name in the message, then click Send.