The Week In Review 06/09/25

“I like the dreams of the future better than the history of the past.” – Thomas Jefferson

Good Morning ,

There was a lot of drama in the market last week, the most prominent of which was the reconciliation bill feud between Elon Musk and President Trump that blew up on Thursday, triggering a 14.3% decline in Tesla's stock price.

All is not well in Camelot!

Fortunately, none of that really distracted the stock market, which enjoyed another winning week behind the leadership of the small-cap stocks and mega-cap stocks.

There were a lot of gains to go around, including NVIDIA and the semiconductor stocks pacing the pack.

The week ended on a high note… as the S&P 500 reclaimed the 6,000 level in the wake of a pleasing employment report for May.

It did so with Treasury yields rising sharply, suggesting perhaps that some rebalancing out of bonds and into stocks might have been providing a tailwind.

The communication services (+3.2%), information technology (+3.0%), and energy (+2.2%) sectors were the best-performing sectors last week. The consumer staples (-1.6%), utilities (-1.1%), and consumer discretionary (-0.6%) sectors were the only sectors that did not show a gain for the week.

In any case… the stock market did not look overly concerned on Friday as the 10-yr note yield rose to 4.51%.

The May employment report was a welcome end to a week that was filled with notable macro developments:

- OPEC+ agreed to raise production by 411,000 barrels per day in July.

- The OECD downgraded its 2025 global GDP growth forecast to 2.9% from 3.1% and its U.S. GDP growth forecast to 1.6% from 2.2%.

- President Trump said that President Xi is "very tough, and extremely hard to make a deal with." That view preceded a phone call between the two leaders, a summary of which sounded more conciliatory than combative and included an agreement to have their respective trade teams meet again soon.

- The ADP Employment Change Report for May indicated that there were only 37,000 jobs added to private-sector payrolls (consensus 115,000) and none for small businesses, which lost 13,000 jobs.

- The ISM Services PMI for May printed a contractionary reading (49.9%) for only the fourth time in the last 60 months.

- Elon Musk decried the one big, beautiful bill on social media and urged lawmakers to "kill the bill."

- The European Central Bank voted to cut its key interest rates by 25 basis points, as expected, and officials suggested that might be the end of the rate cuts.

- The trade deficit plunged in April to $61.6 billion (consensus: -$117.2 billion) from an upwardly revised deficit of $138.3 billion (from -$140.5 billion) in March. Exports were $8.3 billion more than March exports, but imports were $68.4 billion less than March imports.

- President Trump said his top trade representatives, who include Treasury Secretary Bessent, Commerce Secretary Lutnick, and U.S. Trade Representative Greer, will meet Monday in London with representatives from China in reference to the trade deal.

- The May employment report was better than feared and frankly good enough to lend confidence to the idea that the U.S. economy has enough labor market footing to remain on a growth trajectory.

Much to digest!

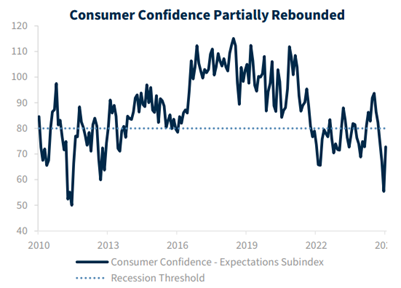

Consumer Confidence has been a metric closely watched…

Source: Raymond James Equity Research

Consumer spending is paramount to the health of our economy!

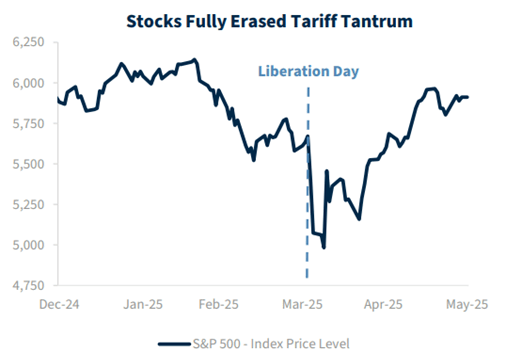

Volatility has been unprecedented in 2025…

Source: Raymond James Equity Research

Often, the best strategy is to not do anything… and to stay with our investment plan, ignoring the noise and distraction.

Deciding to NOT do anything is an absolute decision, many investors sold in the April crash… will they buy back in?

Have a fantastic week!!

The opinions expressed herein are those of Michael Hilger and not necessarily those of Raymond James & Associates, Inc., and are subject to change without notice. The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. There is no assurance any of the trends mentioned will continue or forecasts will occur. The information has been obtained from sources considered to be reliable, but Raymond James does not guarantee that the foregoing material is accurate or complete. Investing involves risk and you may incur a profit or loss regardless of strategy selected.

The information contained herein is general in nature and does not constitute legal or tax advice. Inclusion of these indexes is for illustrative purposes only. Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs or other fees, which will affect actual investment performance. Individual investor's results will vary. Past performance does not guarantee future results. The Dow Jones Industrial Average (INDU) is the most widely used indicator of the overall condition of the stock market, a price-weighted average of 30 actively traded blue chip stocks, primarily industrials. The Dow Jones Transportation Average (DJTA, also called the "Dow Jones Transports") is a U.S. stock market index from the Dow Jones Indices of the transportation sector, and is the most widely recognized gauge of the American transportation sector. Standard & Poor's 500 (SPX) is a basket of 500 stocks that are considered to be widely held. The S&P 500 index is weighted by market value, and its performance is thought to be representative of the stock market as a whole. The S&P 500 is an unmanaged index of widely held stocks that is generally representative of the U.S. stock market. Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs and other fees, which will affect investment performance. Individual investor’s results will vary. The NASDAQ Composite Index (COMP.Q) is an index that indicates price movements of securities in the over-the-counter market. It includes all domestic common stocks in the NASDAQ System (approximately 5,000 stocks) and is weighted according to the market value of each listed issue. The NASDAQ-100 (^NDX) is a modified capitalization-weighted index. It is based on exchange, and it is not an index of U.S.-based companies. The Russell 2000 index is an unmanaged index of small cap securities which generally involve greater risks.

U.S. government bonds and Treasury notes are guaranteed by the U.S. government and, if held to maturity, offer a fixed rate of return, and guaranteed principal value. U.S. government bonds are issued and guaranteed as to the timely payment of principal and interest by the federal government. Treasury notes are certificates reflecting intermediate-term (2 - 10 years) obligations of the U.S. government.

The companies engaged in business related to a specific sector are subject to fierce competition and their products and services may be subject to rapit obsolescence. There are additional risks associated with investing in an individual sector, including limited diversification.

Dividends are not guaranteed and must be authorized by the company's board of directors.

Diversification does not ensure a profit or guarantee against a loss.

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website's users and/or members.

Investing in oil involves special risks, including the potential adverse effects of state and federal regulation and may not be suitable for all investors.

International investing involves special risks, including currency fluctuations, differing financial accounting standards, and possible political and economic volatility.

The companies engaged in the communications and technology industries are subject to fierce competition and their products and services may be subject to rapid obsolescence.

Gold is subject to the special risks associated with investing in precious metals, including but not limited to: price may be subject to wide fluctuation; the market is relatively limited; the sources are concentrated in countries that have the potential for instability; and the market is unregulated.

The information contained within this commercial email has been obtained from sources considered reliable, but we do not guarantee the foregoing material is accurate or complete.

Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Prior to making an investment decision, please consult with your financial advisor about your individual situation.

Charts are reprinted with permission, further reproduction is strictly prohibited.

If you would like to be removed from this e-Mail Alert Notification, PLEASE click the Reply button, type "remove" or "unsubscribe" in the subject line and include your name in the message, then click Send.