The economy's case for lower rates

Chief Economist Eugenio J. Alemán discusses current economic conditions.

We disagree with the way the current administration is pressuring the Federal Reserve (Fed) to lower interest rates because lowering rates must not be a political decision; it must stand on its own economic and monetary policy merits. Doing otherwise risks de-anchoring inflationary expectations, threatening the objectives of low and stable inflation. There are plenty of historical examples across the global economy (Argentina and Turkey), of the risks of losing central bank independence from the political process and what it means for inflation as well as for the value of that country’s currency.

Our first economic argument is that the Fed’s tight monetary policy was not the most important factor in bringing inflation down after its onset, as the economy recovered from the pandemic. The Fed’s monetary policy stance probably did contribute to keeping inflation expectations relatively anchored, but inflation came down as excess savings accumulated during the pandemic dwindled and as pandemic supply chain disruptions came to an end.

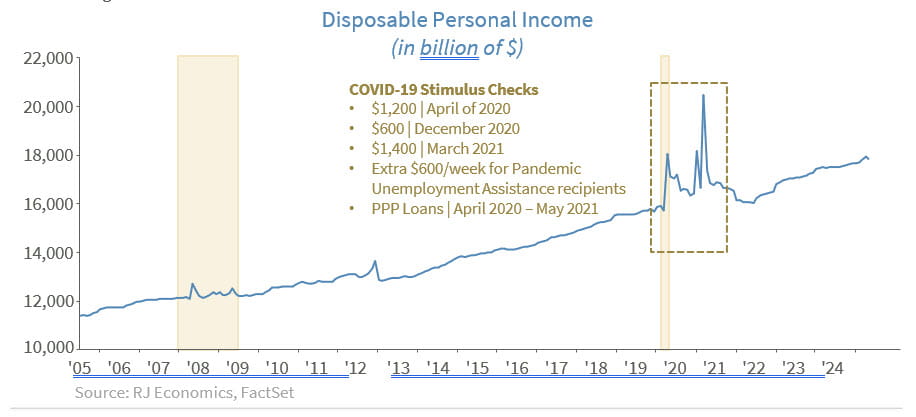

Second, the Fed had to keep interest rates high because the economy was growing above potential due to several factors. As we said above, Americans had accumulated plenty of excess savings and had been unloading them at will and a fast pace, pushing economic growth higher. At the same time, the Biden administration added three stimulus packages through the passing of three acts that pushed investment in new manufacturing plants and fiscal expenditures higher: the CHIPS Act, the IRA, and the Infrastructure Act. Thus, the Fed needed to conduct countercyclical monetary policy, i.e., high interest rates, to limit the potential inflationary effects coming from expansionary fiscal policies, adding upward pressure to economic growth.

Third, the underlying forces behind the disinflationary process are still at play, and although there are risks of higher inflation in the coming quarters, the Fed has to start worrying about what is going to happen 12 months from now. There will be plenty of opportunities to worry about inflation and raise interest rates later.

Tariffs are going to push inflation higher, but the size of the increase in prices is unknown today. First, nobody knows how high tariffs are going to go. Second, economic growth is weakening, so the pass- through from tariffs to prices may not be as high as originally thought. Third, although there are signs that tariffs are pushing prices higher, the actual impact is still limited. This could mean that, at least for now, firms and importers may be ‘eating,’ as President Trump suggested firms should do, a higher percentage of the increase in tariffs, or have been able to negotiate down prices with suppliers, and/or are reluctant to pass higher prices to the final consumer.

The Fed’s latest Beige Book makes several references to various strategies pursued by companies with regard to tariffs. Some of these are:

- Passing costs to customers: Some companies just raise their prices to cover the extra cost from tariffs.

- Delaying price hikes: Others are waiting to raise prices because they still have a lot of inventory that was bought before the tariffs went up.

- Adding surcharges: Instead of changing the base price, some companies add a separate fee (a surcharge) to cover the tariff.

- Sharing the cost: Some split the extra cost between their suppliers and customers, so no one bears the full burden.

- Absorbing the cost: In highly competitive markets, some companies don’t raise prices at all, fearing they’ll lose customers.

- Raising prices on unrelated goods: Some companies increase prices on other products that aren’t affected by tariffs, especially if those products are things people will buy no matter what (inelastic demand), to make up for losses elsewhere.

That is, so far, the impact is still to be felt, and uncertainty remains. However, alongside all this uncertainty, life goes on, and the economy continues to slow down, which should be enough to make Fed members second guess the current path for interest rates. But more importantly, the fights we have to fight cannot wait because we are uncertain about the future. Whatever we need to do today to fix things, we have to do now because we do not know what we do not know. What the Fed knows today is that the disinflationary process remains in place, and inflation is close to the institution’s 2.0% target. In this environment, holding back policy tools in anticipation of an uncertain future event is a risk we can’t afford. Therefore, we believe the Fed should act based on the data it has today and not on speculation about a fight that may never come. Furthermore, lowering the fed funds rate (short-term rate) does not guarantee that longer-term rates come down, as we have seen since the Fed started to lower rates during this latest cycle.

After the pandemic, the Fed decided to wait further because that was one of the lessons learned after the Great Recession, as the deflationary environment pushed it to the ‘zero lower bound’ strategy.

But the Fed missed the fact that the post-pandemic environment was not similar to the post-Great Recession environment. In the post-pandemic case, it was wrong to wait. However, going back, it would have been politically catastrophic to increase interest rates during the recovery from the pandemic recession.

Today, the Fed is waiting too long, and again it is risking being wrong. In any case, it can lower rates today, and if it has to increase rates later, there is nothing that can keep the Fed from doing so. Inflation will continue to go up because of tariffs, but the slowdown in economic activity will keep the increase in inflation limited. However, if the Fed continues to keep rates at these levels, it risks the economy going into recession. It is not a decision Fed officials take lightly, and they shouldn’t. They must make the decision on its merits, and there are some reasons to lower rates slightly today.

Perhaps the biggest risk for the Fed today is the effects of the fiscal expansion coming from the One Big Beautiful Bill Act (OBBBA), which is, for the most part, front-loaded, and could push economic growth higher. However, the potential effects of lowering taxes are not straightforward because firms and individuals could spend those extra funds, but have the freedom to pay back debt and/or save the extra funds, which limits the impact on economic growth.

Once again, we disagree with the administration’s strategy to push the Fed to lower rates by 100 or 200 basis points, as we have heard several times. These are politically motivated arguments that are not based on what the economy requires and are highly counterproductive because Fed members take a defensive stance to avoid making a decision that could be construed as being politically motivated. However, there are many economic arguments that are pointing to lower interest rates, at least in the short run, to front- run further weakness in economic activity. Furthermore, we know that political intervention could keep the Fed on the sidelines because it fears that economic agents would consider these moves ‘politically motivated.’ However, Fed officials know what is best for the economy and where the economy seems to be heading and should do what is necessary to keep the economy going. If the Fed continues to follow economic arguments rather than politically motivated pressure coming from the administration, the risks to unleashing higher inflation expectations will remain low.

Economic and market conditions are subject to change.

Opinions are those of Investment Strategy and not necessarily those of Raymond James and are subject to change without notice. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There is no assurance any of the trends mentioned will continue or forecasts will occur. Past performance may not be indicative of future results.

Consumer Price Index is a measure of inflation compiled by the US Bureau of Labor Statistics. Currencies investing is generally considered speculative because of the significant potential for investment loss. Their markets are likely to be volatile and there may be sharp price fluctuations even during periods when prices overall are rising.

Consumer Sentiment is a consumer confidence index published monthly by the University of Michigan. The index is normalized to have a value of 100 in the first quarter of 1966. Each month at least 500 telephone interviews are conducted of a contiguous United States sample.

Personal Consumption Expenditures Price Index (PCE): The PCE is a measure of the prices that people living in the United States, or those buying on their behalf, pay for goods and services. The change in the PCE price index is known for capturing inflation (or deflation) across a wide range of consumer expenses and reflecting changes in consumer behavior.

The Consumer Confidence Index (CCI) is a survey, administered by The Conference Board, that measures how optimistic or pessimistic consumers are regarding their expected financial situation. A value above 100 signals a boost in the consumers’ confidence towards the future economic situation, as a consequence of which they are less prone to save, and more inclined to consume. The opposite applies to values under 100.

Certified Financial Planner Board of Standards Center for Financial Planning, Inc. owns and licenses the certification marks CFP®, CERTIFIED FINANCIAL PLANNER®, and CFP® (with plaque design) in the United States to Certified Financial Planner Board of Standards, Inc., which authorizes individuals who successfully complete the organization’s initial and ongoing certification requirements to use the certification marks.

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website's users and/or members.

GDP Price Index: A measure of inflation in the prices of goods and services produced in the United States. The gross domestic product price index includes the prices of U.S. goods and services exported to other countries. The prices that Americans pay for imports aren't part of this index.

Employment cost Index: The Employment Cost Index (ECI) measures the change in the hourly labor cost to employers over time. The ECI uses a fixed “basket” of labor to produce a pure cost change, free from the effects of workers moving between occupations and industries and includes both the cost of wages and salaries and the cost of benefits.

US Dollar Index: The US Dollar Index is an index of the value of the United States dollar relative to a basket of foreign currencies, often referred to as a basket of U.S. trade partners' currencies. The Index goes up when the

U.S. dollar gains "strength" when compared to other currencies.

Import Price Index: The import price index measure price changes in goods or services purchased from abroad by U.S. residents (imports) and sold to foreign buyers (exports). The indexes are updated once a month by the Bureau of Labor Statistics (BLS) International Price Program (IPP).

ISM Services PMI Index: The Institute of Supply Management (ISM) Non-Manufacturing Purchasing Managers' Index (PMI) (also known as the ISM Services PMI) report on Business, a composite index is calculated as an indicator of the overall economic condition for the non-manufacturing sector.

Consumer Price Index (CPI) A consumer price index is a price index, the price of a weighted average market basket of consumer goods and services purchased by households.

Producer Price Index: A producer price index(PPI) is a price index that measures the average changes in prices received by domestic producers for their output.

Industrial production: Industrial production is a measure of output of the industrial sector of the economy. The industrial sector includes manufacturing, mining, and utilities. Although these sectors contribute only a small portion of gross domestic product, they are highly sensitive to interest rates and consumer demand.

The NAHB/Wells Fargo Housing Opportunity Index (HOI) for a given area is defined as the share of homes sold in that area that would have been affordable to a family earning the local median income, based on standard mortgage underwriting criteria.

Conference Board Coincident Economic Index: The Composite Index of Coincident Indicators is an index published by the Conference Board that provides a broad-based measurement of current economic conditions, helping economists, investors, and public policymakers to determine which phase of the business cycle the economy is currently experiencing.

Conference Board Lagging Economic Index: The Composite Index of Lagging Indicators is an index published monthly by the Conference Board, used to confirm and assess the direction of the economy's movements over recent months.

New Export Index: The PMI New export orders index allows us to track international demand for a country's goods and services on a timely, monthly, basis.

Gold is subject to the special risks associated with investing in precious metals, including but not limited to: price may be subject to wide fluctuation; the market is relatively limited; the sources are concentrated in countries that have the potential for instability; and the market is unregulated.

The Conference Board Leading Economic Index: Intended to forecast future economic activity, it is calculated from the values of ten key variables.

Source: FactSet, data as of 12/6/2024