The Week in Review 7/31/2023

“The two most powerful warriors are patience and time.” - Leo Tolstoy

Last week gave us much to digest… earnings, economic, and central bank news.

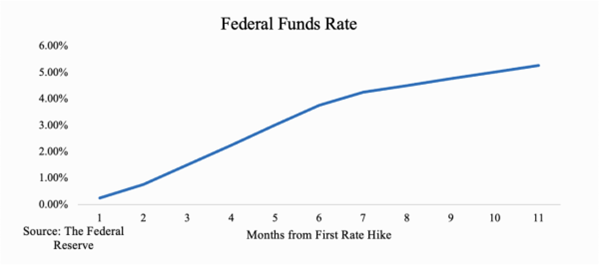

Investors continue to marvel at the resiliency of the US economy, despite the relentless work of the Fed raising rates to a 22 year high! We expect that the Fed is close to being done raising rates.

There is also much anticipation that earnings growth will accelerate in the second half of the year.

The FOMC voted unanimously on Wednesday to raise the target range for the fed funds rate by 25 basis points to 5.25-5.50%, as expected.

The policy directive also upgraded the description of economic activity to expanding at a moderate pace, from continuing to expand at a modest pace in the June directive.

Expectations for a pause on September 20th are high…. According to the CME FedWatch Tool, probability of a second rate hike at any of the remaining FOMC meetings this year remains under 30%.

There are three more FOMC meetings in 2023, the next being September 19 and 20. Current odds, based on the futures market, show an 80% chance of another pause at that time.

There is quite a bit of time between now and then however, with a plethora of economic data to be released, which likely will influence the Fed’s decision.

Fed governor Christopher Waller in a July speech said he wants to see evidence that the latest inflation slowdown wasn’t a fluke. The recent report, he said, “warmed my heart, but…I’ve got to make policy with my head. And I can’t do that on one data point.”

I guess we would call that somewhere between “hawkish” and dovish”?

The ECB followed suit… with a 25 basis points increase in its three key lending rates, although there is some speculation, driven by the language in its directive, that the ECB could also be close to being done raising rates.

The Bank of Japan made no changes to its interest rates… but surprised market participants when it voted to conduct its yield curve control policy with greater flexibility, saying it will maintain the target rate at 0.5%, but will offer to purchase 10-yr JGBs at 1.0% every business day through fixed-rate purchase operations.

Earnings are holding up… especially in Mega Cap Technology.

Microsoft, Alphabet, and Meta Platforms were the most influential movers. Microsoft's results were deemed a little disappointing when its revenue guidance didn't live up to bullish expectations, but it was a good report overall. Alphabet and Meta Platforms both delivered results and/or guidance that triggered some distinctly positive action in their prices.

So far, 51% of companies in the S&P 500 have reported their earnings results.

Of those, 80% have reported earnings of 5.9% above analysts’ estimates, but the blended earnings rate has declined 7.3% for the quarter, according to FactSet.

Those gains, along with earnings-related gains in some blue-chip names like Boeing, McDonald's, and Dow Inc., helped index performance.

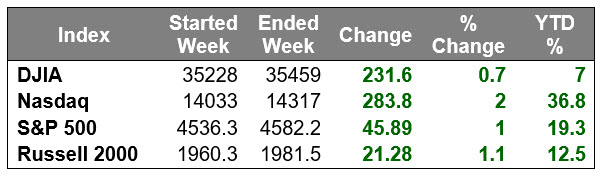

Our markets continue to see a broadening out of the buying interest, although this week's gains were spear headed by the mega cap space.

The S&P 500 communication services sector was the best performer by a wide margin, rising 6.9%, reflecting the strong showing from Meta Platforms and Alphabet. Other top performers included the materials (+1.8%) and energy (+1.7%) sectors. Meanwhile, the utilities (-2.1%) and real estate (-1.8%) sectors saw the biggest declines.

Last week also featured a series of economic reports that continue to validate the soft landing/no landing view. There was an uptick in consumer confidence, which was driven both by a pickup in views about current conditions and the outlook, another low level of weekly initially jobless claims, and a strong than expected 2.4% increase in Q2 GDP, which was up from 2.0% in Q1.

Rounding out the econ calendar was the June Personal Income and Spending Report, which showed solid spending and ongoing disinflation.

Market Snapshot…

- Oil Prices – Oil prices were steady on Friday but on track for a fifth straight week of gains. West Texas Intermediate crude (WTI) dipped 3 cents to $80.06 a barrel. Brent crude futures slipped 9 cents to $84.15 a barrel.

- Gold– Gold headed for its worst week in five. Spot Gold rose 0.6% to $1,956.69 per ounce by 1133 GMT, up from its lowest since July 12. U.S. gold futures gained 0.5% to $1,955.70. Silver finished the week at $24.495.

- U.S. Dollar– The dollar fell against a basket of its major peers as investors largely shrugged off new data showing inflation slowing. The dollar index fell 0.138% to 101.530. Euro/US$ exchange rate is now 1.107.

- U.S. Treasury Rates– The yield on the 10-year Treasury was trading at 3.957% after falling by more than 5 basis points.

- Asian shares were up in overnight trading.

- European markets are trading higher.

- Domestic markets are trading modestly this morning.

This week will be even busier in term of earnings news… there's also some market-moving economic data in the form of the ISM Manufacturing and Services Indexes and the July Employment Report.

Earnings season is in full swing, and we'll hear from over 30% of the S&P this week.

Have a fantastic week!

The opinions expressed herein are those of Michael Hilger and not necessarily those of Raymond James & Associates, Inc., and are subject to change without notice. The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. There is no assurance any of the trends mentioned will continue or forecasts will occur. The information has been obtained from sources considered to be reliable, but Raymond James does not guarantee that the foregoing material is accurate or complete. Investing involves risk and you may incur a profit or loss regardless of strategy selected.

The information contained herein is general in nature and does not constitute legal or tax advice. Inclusion of these indexes is for illustrative purposes only. Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs or other fees, which will affect actual investment performance. Individual investor's results will vary. Past performance does not guarantee future results. The Dow Jones Industrial Average (INDU) is the most widely used indicator of the overall condition of the stock market, a price-weighted average of 30 actively traded blue chip stocks, primarily industrials. The Dow Jones Transportation Average (DJTA, also called the "Dow Jones Transports") is a U.S. stock market index from the Dow Jones Indices of the transportation sector, and is the most widely recognized gauge of the American transportation sector. Standard & Poor's 500 (SPX) is a basket of 500 stocks that are considered to be widely held. The S&P 500 index is weighted by market value, and its performance is thought to be representative of the stock market as a whole. The NASDAQ Composite Index (COMP.Q) is an index that indicates price movements of securities in the over-the-counter market. It includes all domestic common stocks in the NASDAQ System (approximately 5,000 stocks) and is weighted according to the market value of each listed issue. The Russell 2000 index is an unmanaged index of small cap securities which generally involve greater risks.

Dividends are not guaranteed and must be authorized by the company's board of directors.

Diversification does not ensure a profit or guarantee against a loss.

Investing in oil involves special risks, including the potential adverse effects of state and federal regulation and may not be suitable for all investors.

International investing involves special risks, including currency fluctuations, differing financial accounting standards, and possible political and economic volatility.

The companies engaged in the communications and technology industries are subject to fierce competition and their products and services may be subject to rapid obsolescence.

Gold is subject to the special risks associated with investing in precious metals, including but not limited to: price may be subject to wide fluctuation; the market is relatively limited; the sources are concentrated in countries that have the potential for instability; and the market is unregulated.

The information contained within this commercial email has been obtained from sources considered reliable, but we do not guarantee the foregoing material is accurate or complete.

Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Prior to making an investment decision, please consult with your financial advisor about your individual situation.

Charts are reprinted with permission, further reproduction is strictly prohibited.